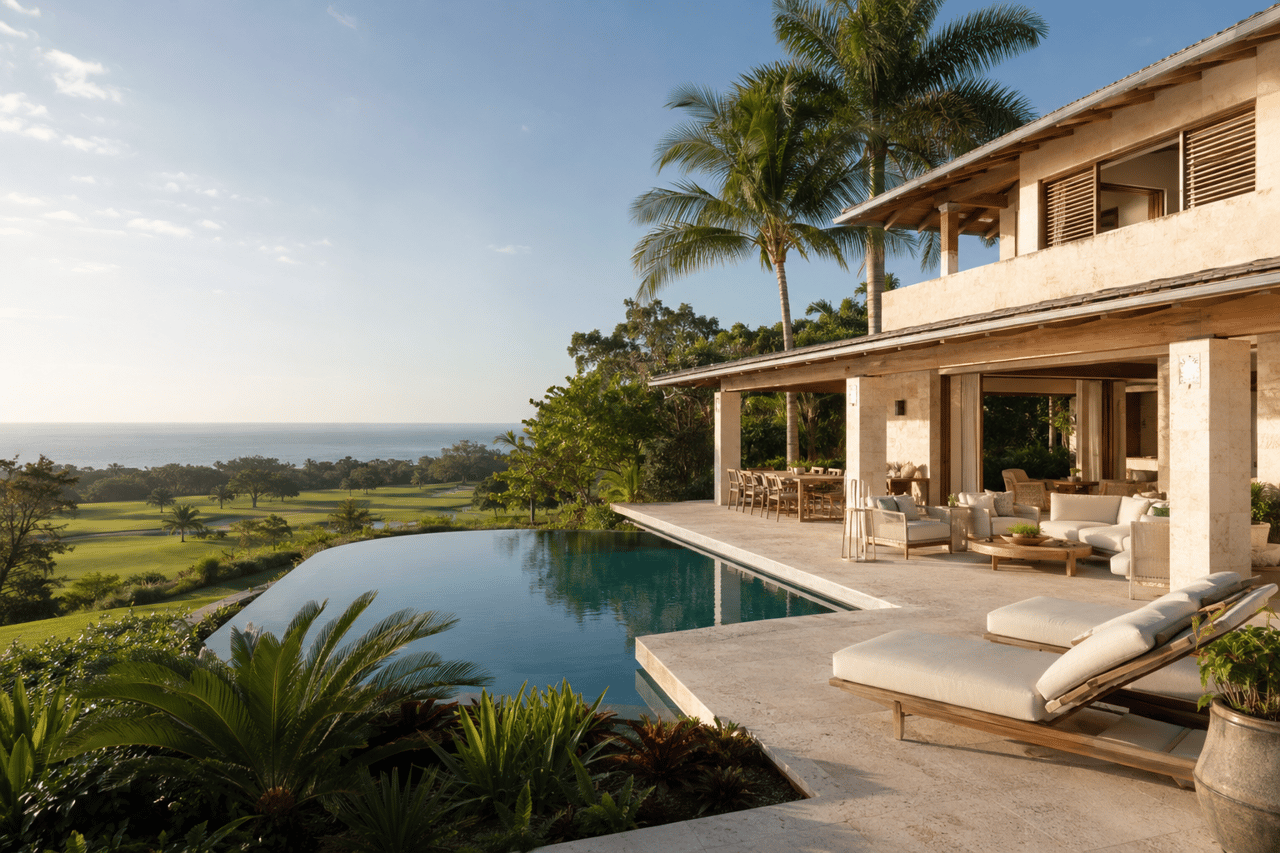

Dreaming of an ocean-view condo in Condado but not sure what to check beyond the view? You are not alone. Condado’s beachfront location, vibrant mix of residents and visitors, and older building stock create a unique set of questions for buyers. In this guide, you will learn the exact documents, inspections, insurance details, and rules to review so you can buy with confidence. Let’s dive in.

Why Condado condos are different

Condado sits right on the coast, which means salt spray, humidity, and tropical storms are part of daily life. These conditions speed up corrosion on metal, balconies, window systems, and railings, and they increase the need for regular exterior maintenance and capital projects. Wind and flood exposure also shape insurance needs and costs.

Inventory ranges from mid-century low-rises to fully renovated towers and newer luxury high-rises. Many buildings include full-time residents, seasonal owners, and some vacation rental activity. This mix affects maintenance patterns, reserve planning, staffing, and house rules.

There is also a regulatory overlay. FEMA flood maps influence flood insurance requirements. Local permitting and property registration rules interact with how buildings enforce leasing, short-term rentals, and tourism tax obligations. You will also see common buyer concerns in Condado like frequent assessments in older buildings, higher storm deductibles, rental restrictions, limited garage parking, and noise or amenity access pressure in tourist seasons.

Review these condo documents

A strong offer starts with the right documents. Ask for a full condo pack and review the sections below before you commit.

Governing documents

These include the Declaration or Master Deed, Bylaws, Rules and Regulations, and any amendments or house rules. You will find unit boundaries, common elements, voting thresholds, and rules on leasing, pets, parking, guests, and assessments.

- Look for: minimum lease terms, caps on rentals, owner-occupancy requirements, and board authority to levy special assessments.

- Red flags: rules that ban your intended use, broad discretionary powers without clear limits, or recent amendments that add new costs.

Association financials

Study the current operating budget, balance sheet, income and expense trends, cash on hand, and a delinquency report. Ask whether statements are audited or reviewed.

- Look for: a clear budget, stable dues, and manageable delinquencies.

- Red flags: recurring operating deficits, rising delinquencies, no working capital, or multiple recent dues increases without a clear reason.

Reserves and capital planning

You want a recent reserve study or engineer’s report that covers the roof, façade, elevators, waterproofing, plumbing risers, and common-area systems. Compare the reserve balance to recommended funding.

- Why this matters in Condado: coastal conditions shorten the useful life of balconies, façade sealants, roofs, and windows. Underfunded reserves often lead to special assessments.

Assessments and claims

Review recent or upcoming special assessments and why they were levied. Ask for insurance claims history for the last 5 to 10 years, plus any pending repair projects and timelines.

- Red flags: frequent assessments, large unresolved claims, litigation tied to assessments, or projects without clear contracts and schedules.

Minutes, governance, and litigation

Read board meeting minutes for the last 12 to 24 months. You will see discussions on repairs, enforcement, staffing, and assessments. Confirm any pending or threatened litigation and review the management contract for experience and termination terms.

- Red flags: patterns of deferred maintenance, major disputes, developer transition issues, or building-wide litigation that could lead to future costs.

Insurance you must verify

In Condado, insurance can make or break the numbers. Verify what the association’s policy covers and where you need your own coverage.

Master policy basics

Request the master insurance declaration and confirm what is included. Check policy limits, per-occurrence deductibles, and named-storm or windstorm deductibles. Some policies include an assessable deductible clause, which can make owners responsible for part of a large deductible after a covered loss.

- Red flags: very high hurricane or wind deductibles based on a percentage of building value, low policy limits, or unclear loss-assessment rules.

Flood considerations

Confirm whether the building carries flood coverage and the extent of that coverage. If a unit is in a FEMA Special Flood Hazard Area and the association does not hold adequate flood insurance, many lenders will require owner flood policies.

Your HO-6 policy

Most owners need an HO-6 policy for interior finishes, personal property, loss assessment, and liability. Some associations require specific minimums or proof of loss assessment coverage. Coordinate your HO-6 with the master policy so there are no gaps.

Inspect building condition

Coastal buildings deserve extra scrutiny. Do not skip expert inspections.

Structural and engineering

Order a structural or engineering review when a building shows signs of corrosion, cracking, settlement, or water intrusion. In seaside settings, hidden corrosion can weaken rebar and balcony components over time.

Roof and façade

Request recent roof and façade inspection reports. Look for evidence of leaks, failing sealants, cracked tile, or spalling concrete. Ask about waterproofing cycles and timelines for planned work.

Plumbing and electrical

Note the age and material of plumbing risers, and confirm any past water damage repairs. In older towers, galvanized piping may be at the end of its useful life. Check electrical capacity and panel updates within units and common areas.

Elevators and life safety

Review elevator maintenance records and any modernization plans. Confirm life safety systems and inspection cycles are current, especially in taller buildings.

Moisture and HVAC

Humidity and mold are common in coastal environments. Order a moisture and HVAC inspection at the unit level. Ask how the building manages humidity in common areas and whether there have been recurring mold issues.

Rules that affect your lifestyle

Before you picture your routine, confirm the rules that shape daily life in the building.

Parking and storage

Identify the type of parking right included with the unit. A deeded stall offers stronger rights than an assigned license. Ask about availability for a second car, guest parking, and any monthly parking fees. Street parking near the beach can be limited or metered.

- Buyer questions: Is parking included? Is the stall deeded or assigned? Is there a waitlist for extra spaces?

Pets and service animals

Confirm pet policies, including size, number, or breed limits, and any registration rules. Keep in mind that federal fair housing rules generally require reasonable accommodation for service and assistance animals. These protections apply in Puerto Rico.

Rentals and short-term use

Many associations set minimum lease terms, cap rental percentages, or ban short-term rentals. Local registration and tourism taxes may apply for rentals, but a building can still prohibit them. High rental ratios can affect financing and insurance for buyers.

- Buyer questions: Are short-term rentals allowed? What is the minimum lease term? Is there a cap on rented units?

Amenities, security, and staffing

Check hours and rules for pools, gyms, and terraces, especially in tourist-heavy areas. Ask about front desk staffing, cameras, and controlled access. Review how staffing appears in the budget and whether roles are contractors or employees.

Smart offer to closing timeline

Map your steps before you write the offer. A clear plan helps you negotiate and protects your deposit.

Pre-offer prep

- Request a preliminary condo pack with governing documents, recent minutes, budget, reserve study, master insurance certificate, and a list of recent or planned assessments.

- Ask key questions on pending assessments, rental ratios, and any litigation items.

- Confirm parking rights and whether storage is included.

Offer to contract

Include condo-specific contingencies, such as:

- Review and approval of condo documents within a set period.

- Review of financials, reserve study, and master insurance.

- Structural, moisture, and unit-level inspections.

- Confirmation of no pending assessments or acceptable terms for disclosed ones.

- Financing contingency that accounts for condo restrictions lenders may impose.

During inspection and escrow

- Hire a unit-level inspector with moisture expertise.

- Bring in a structural or façade engineer if you see corrosion or recent major repairs.

- Ask an insurance broker to quote HO-6 and review loss-assessment exposure.

- Work with a local condo attorney for title review, deed description, parking deed if applicable, and any encumbrances.

- Request a certificate of good standing from the association and a certification of payments for the unit, if available.

Closing checklist

- Confirm any required board approvals and transfer fees.

- Ask for updated minutes or notices issued after contract acceptance.

- Clarify who pays any new assessment voted after the contract date based on your agreement and local rules.

- Arrange utility transfers, access cards, keys, gate remotes, and parking tags.

The right local team

A knowledgeable local agent can save you time and lower risk. The right advisor knows building managers, understands typical document turnaround times, and can pre-screen buildings for common Condado issues like age-related repairs, hurricane claims, and frequent assessments. They can coordinate the right professionals, including condo attorneys, engineers, inspectors with moisture expertise, insurance brokers who understand wind and flood products, and tax professionals if you plan to rent the unit.

Key red flags to pause on

- High or growing delinquencies paired with low reserves.

- Recent or recurring special assessments without a funded plan.

- Large pending litigation involving the association or developer.

- Extremely high named-storm deductibles likely to be assessed to owners.

- Evidence of water intrusion, corrosion, or structural issues without a repair plan.

- Rules that restrict the way you intend to use the unit, such as rentals, pets, or parking.

A simple buyer takeaway

Condado rewards careful buyers. If you verify master insurance and flood exposures, confirm reserve funding against coastal maintenance needs, review bylaws for rental, pet, and parking limits, and order focused structural and moisture inspections, you will reduce surprises. Pair that with a local agent and condo attorney who can obtain and interpret building-level documents, and you will be ready to act with confidence.

Ready to explore your options in Condado? Connect with the team that blends high-touch brokerage with clear, education-first guidance. Reach out to INCANTO Real Estate & Relocation to Book Your Call.

FAQs

What makes buying a Condado condo different?

- Coastal exposure increases corrosion and storm risk, which drives stricter insurance needs, more frequent exterior projects, and closer review of reserves and assessments.

Do Condado condos require flood insurance?

- Flood needs depend on FEMA mapping and the building’s coverage; if a unit is in a Special Flood Hazard Area and the association lacks adequate flood coverage, many lenders will require an owner flood policy.

Can I use my Condado condo for short-term rentals?

- It depends on the building’s rules, which may set minimum lease terms, cap rental ratios, or prohibit short-term rentals even if local registration is available.

How do special assessments affect buyers?

- Special assessments raise owner costs and can be triggered by capital projects or insurance deductibles; confirm amounts, timelines, and who is responsible before closing.

What should I confirm about parking in Condado?

- Verify whether a stall is deeded or assigned, whether a second space is possible, any monthly fees, and the status of guest or street parking near the building.